Buying a car is rarely just about choosing a model or a color. For most people—and even for CEOs and high-level professionals—it is a financial decision that deserves careful thought. The way you finance your car can impact your cash flow, tax planning, credit profile, and long-term financial flexibility.

Car financing today offers more options than ever before. From traditional bank loans to leasing, dealer financing, and emerging digital platforms, each option comes with its own advantages and trade-offs. The challenge is not a lack of choice, but understanding which option aligns best with your financial goals and lifestyle.

This guide is written for decision-makers who value clarity, efficiency, and smart financial strategy. Whether you are purchasing your first vehicle, upgrading your executive car, or managing a company fleet, this article will help you navigate your options in car financing with confidence.

Understanding Car Financing: The Big Picture

Car financing simply means paying for a vehicle over time rather than upfront. While that sounds straightforward, the structure of financing can vary significantly.

At its core, car financing answers three questions:

- How much are you borrowing or committing to pay?

- How long will the payment period last?

- What will the total cost be after interest, fees, and depreciation?

For executives and business owners, an additional layer comes into play: opportunity cost. Capital tied up in a depreciating asset like a car is capital that could otherwise be invested in a growing business or financial portfolio.

Understanding the mechanics behind each financing option is the first step toward making a smart decision.

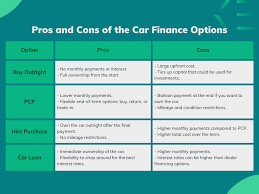

Paying Cash: The Simplest Option with Hidden Costs

Paying cash for a car is often seen as the cleanest and safest option. No interest, no monthly payments, no long-term obligations. On the surface, it feels financially responsible.

Advantages of Paying Cash

- Full ownership from day one

- No interest or financing fees

- No credit checks or approvals

- Strong negotiating position with dealers

The Hidden Trade-Offs

However, paying cash is not always the smartest move, especially for high-income earners or CEOs. Cars depreciate quickly. In many cases, investing that cash elsewhere could yield higher returns than the interest you would pay on a loan.

There is also liquidity to consider. Keeping cash available provides flexibility for emergencies, investments, or business opportunities. Once cash is spent on a car, it is locked into an asset that loses value over time.

For some, peace of mind outweighs these concerns. For others, especially those focused on growth and leverage, cash may not be the optimal choice.

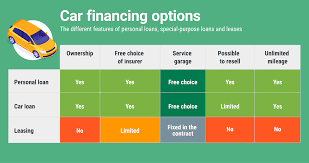

Bank Auto Loans: Traditional but Reliable

Bank auto loans remain one of the most common car financing options. They offer predictability, transparency, and often competitive interest rates—especially for borrowers with strong credit profiles.

How Bank Loans Work

You borrow a fixed amount, agree to a repayment term (typically 36 to 72 months), and make monthly payments that include principal and interest. Once the loan is paid off, the car is yours.

Why Executives Choose Bank Loans

- Clear loan structure and terms

- Lower interest rates for strong credit

- Freedom to choose any dealer or seller

- No mileage restrictions

Potential Downsides

- Requires a solid credit score

- Approval process can take time

- Monthly payments affect cash flow

- Car is used as collateral

For many professionals, a bank loan strikes the right balance between ownership and financial flexibility.

Dealer Financing: Convenience with Caution

Dealer financing is often the easiest option at the point of sale. Everything happens in one place, sometimes within hours.

Why Dealer Financing Is Attractive

- Fast approval process

- Promotional offers (0% APR, cashback deals)

- Simplified paperwork

- Flexible options for buyers with varied credit profiles

What to Watch Out For

Dealer financing can sometimes include higher interest rates, hidden fees, or longer loan terms that increase the total cost of ownership. Promotional rates may only apply to specific models or require excellent credit.

For CEOs who value time efficiency, dealer financing can make sense—but only after comparing it with external loan offers.

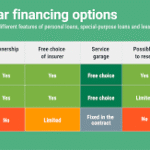

Leasing a Car: Strategic Flexibility for Modern Professionals

Leasing has become increasingly popular among executives, especially those who prefer driving newer vehicles and minimizing long-term commitments.

How Leasing Works

You essentially pay for the depreciation of the car during the lease term, plus interest and fees. At the end of the lease, you can return the car, buy it, or upgrade to a new model.

Benefits of Leasing

- Lower monthly payments compared to buying

- Access to newer models and technology

- Warranty coverage throughout the lease

- Potential tax benefits for business use

Limitations to Consider

- Mileage limits

- No ownership unless you buy at the end

- Wear-and-tear charges

- Continuous payment cycle

For executives who see a car as a tool rather than an asset, leasing offers unmatched flexibility.

Balloon Financing: Lower Payments with a Future Decision

Balloon financing combines elements of loans and leasing. Monthly payments are lower because a large “balloon” payment is due at the end of the term.

Why Some Choose Balloon Payments

- Reduced monthly expenses

- Flexibility at the end of the term

- Option to refinance or sell the car later

The Risk Factor

The final balloon payment can be substantial. If market conditions or personal finances change, this can create pressure.

This option works best for individuals with strong financial planning and predictable income streams.

Financing Through Credit Unions: A Hidden Gem

Credit unions often offer competitive rates and personalized service. They are member-focused rather than profit-driven.

Advantages

- Lower interest rates

- Flexible terms

- Personalized service

- Transparent fee structures

Considerations

- Membership requirements

- Limited branch availability

- Slower approval in some cases

For financially disciplined borrowers, credit unions can be one of the best-kept secrets in car financing.

Online and Digital Lenders: The New Age of Financing

Digital lenders have transformed car financing by offering speed, transparency, and convenience.

Why Digital Financing Is Growing

- Fast online approval

- Clear rate comparisons

- Minimal paperwork

- Integration with dealerships

Potential Drawbacks

- Limited customer support

- Less room for negotiation

- Varying lender credibility

For tech-savvy executives, online financing can be both efficient and competitive.

Car Financing for Business Owners and CEOs

When a car is used for business purposes, financing decisions become even more strategic.

Tax Considerations

- Lease payments may be tax-deductible

- Depreciation benefits for purchased vehicles

- Interest deductions in some jurisdictions

Cash Flow Management

Financing can help preserve capital for business growth, marketing, or hiring.

Image and Branding

Vehicles often represent the company brand. Financing allows regular upgrades without major capital outlays.

Choosing the Right Financing Option: A Strategic Framework

To choose the right option, ask yourself:

- Do I value ownership or flexibility?

- How important is cash flow?

- Am I optimizing for tax efficiency?

- How often do I plan to change vehicles?

There is no universal “best” option—only the best option for your situation.

Common Mistakes to Avoid in Car Financing

- Focusing only on monthly payments

- Ignoring total cost of ownership

- Overextending loan terms

- Skipping rate comparisons

- Underestimating depreciation

Smart financing is about long-term clarity, not short-term comfort.

Final Thoughts: Financing as a Strategic Decision

Car financing is not just a consumer decision—it is a strategic one. For CEOs, executives, and professionals, the right financing choice can support broader financial goals, preserve capital, and enhance lifestyle flexibility.

By understanding your options and aligning them with your priorities, you transform car financing from a routine transaction into a smart financial move.

A well-financed car is not just a vehicle—it is a reflection of thoughtful decision-making.

End of article.

Summary:

There are so many car financing options available how do you know which one is right for you? Read on to obtain information about all of the different options available and how to determine which one will provide you with the best benefits.

Keywords:

car, finance, loan, personal, borrow, lending, auto, insurance, purchase, cost, interest

Article Body:

There are so many car financing options available how do you know which one is right for you? Read on to obtain information about all of the different options available and how to determine which one will provide you with the best benefits.

Many people take advantage of an option known as dealer financing. This is when you handle the financing of your new vehicle directly through the lender. Now, that doesn�t necessarily mean you�ll be making your payments directly to the dealer. Usually, they work with a finance company to provide the financing to you. There are definitely some benefits to this option. First, depending on your situation you may be able to obtain extremely low interest rates; in some case you may be able to obtain a zero percent interest rate. In order to obtain this special rate; however, you will need to have excellent credit with no problems. If you have any problems at all on your credit history you will not qualify for the special interest rate although you will probably be able to still obtain a loan; just at a higher rate. When your credit report is not perfect ask yourself whether you could get a better deal at a bank.

Bank financing is an option that is typically available as long as your credit history is good. This means it doesn�t have to be perfect but you shouldn�t have any major flaws either. If you have already worked with the bank in the past this will increase your chances of obtaining a loan. While a bank interest rate may not be as low as what a car dealer can offer for individuals with excellent credit, it may be better than what you could obtain at the dealership if your credit is only �good.�

Another option you may wish to consider is credit union financing. Of course, this option is only available if you belong to a credit union. If you do happen to have a credit union membership; however, the rate available to you may be much better than what you can obtain through a bank or dealership.

These days it is also quite easy to simply go online and surf around for a quote from an online lender. This option has become so popular many lenders are now willing to compete with one another and offer very attractive rates. In the event you do not have perfect credit, this can be a good option for you; just make sure you fully understand all of the terms of the loan before accepting it.

Another option would be to simply borrow the funds from a family member of friend. Of course, this is extremely risky because it could cause problems in your relationship in the event that you run into a problem with the payments. But, if you can�t obtain a loan elsewhere because of credit problems this may be a good option.

Finally, you may wish to consider refinancing your home or taking out a home equity loan in order to finance the cost of your new home. This basically allows you to pay cash for your vehicle with the proceeds of the loan and then paying back the money through the refi loan. In some cases you may be able to get a better interest rate with this route than you would with a traditional bank auto loan. In addition, the interest you pay on the loan is tax deductible. Like other options; however, there are some disadvantages. With this option, be aware that you could be putting your house at risk, not just your car, if you run into a problem and can�t make the payments in the future.

Tinggalkan Balasan