Retirement planning is often treated as something distant—important, but not urgent. Many people assume it is a problem for the future, something they will “figure out later” once their career is more stable or their income is higher.

The reality is very different. Retirement planning is not about age. It is about control. The earlier you plan, the more choices you have. The longer you delay, the fewer options remain.

This guide is designed for professionals, executives, and business owners who want clarity—not complexity. Whether retirement is 30 years away or just around the corner, smart planning today determines how much freedom you will have tomorrow.

What Retirement Really Means Today

Retirement no longer looks the same as it did for previous generations. It is not simply about stopping work at 65 and living quietly.

For many modern professionals, retirement means:

- Financial independence

- Flexibility in how and when you work

- The ability to choose, not be forced

- Security without sacrificing lifestyle

Some will retire early. Others will continue working by choice. The common factor is preparation.

Retirement planning is not about escaping work—it is about owning your time.

Why Retirement Planning Fails for So Many People

Despite good intentions, many people struggle to prepare adequately. The reasons are often emotional, not technical.

1. Procrastination

Retirement feels far away, so action is delayed.

2. Overconfidence

People assume future income will solve everything.

3. Complexity

Too many products, rules, and opinions create paralysis.

4. Lifestyle Inflation

As income grows, spending grows faster.

Even high earners fall into these traps. In fact, higher income often hides the problem longer.

The Power of Starting Early

Time is the most powerful asset in retirement planning. Compound growth rewards patience more than aggressive risk-taking.

Starting early allows you to:

- Contribute less each month

- Take calculated investment risks

- Recover from market volatility

- Build habits instead of pressure

Waiting means:

- Higher contributions

- Less flexibility

- Greater stress

- Fewer second chances

The math is simple. The discipline is not.

Defining Your Retirement Vision

Before discussing numbers, you need clarity.

Ask yourself:

- Where do I want to live?

- How do I want to spend my time?

- What does “enough” actually look like?

- Will I fully retire or transition gradually?

A clear vision turns retirement planning from a vague goal into a concrete strategy.

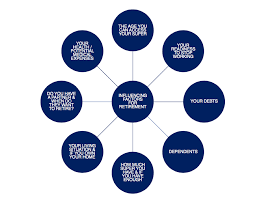

Understanding Retirement Income Sources

A strong retirement plan relies on multiple income streams. Dependence on a single source creates risk.

Common retirement income sources include:

- Personal savings and investments

- Employer-sponsored retirement plans

- Private pension plans

- Business income or equity

- Passive income assets

The goal is balance. Stability comes from diversification.

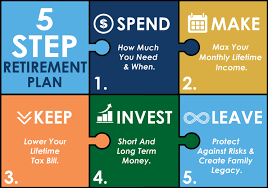

Retirement Savings: How Much Is Enough?

There is no universal number. Retirement needs are personal.

However, a useful framework includes:

- Expected annual living expenses

- Inflation impact over time

- Healthcare costs

- Lifestyle choices (travel, hobbies, family support)

Many planners suggest targeting 70–80% of pre-retirement income, but this is only a starting point. For executives and business owners, lifestyle expectations often require more.

Investing for Retirement: Strategy Over Speculation

Retirement investing is not about beating the market. It is about consistency and risk management.

Key principles include:

- Diversification across asset classes

- Long-term perspective

- Regular contributions

- Periodic rebalancing

Emotional investing is one of the biggest threats to retirement success. Markets fluctuate. Discipline matters more than prediction.

Managing Risk as Retirement Approaches

As retirement gets closer, risk management becomes more important.

This does not mean eliminating risk entirely. It means adjusting exposure:

- Reducing volatility

- Preserving capital

- Protecting income

The transition should be gradual, not abrupt.

Healthcare and Retirement: The Silent Expense

Healthcare is one of the most underestimated retirement costs.

Planning should include:

- Insurance coverage

- Emergency medical funds

- Long-term care considerations

Ignoring healthcare costs can quickly derail an otherwise solid retirement plan.

Retirement Planning for Business Owners and CEOs

For business owners, retirement planning looks different.

Key considerations include:

- Business succession planning

- Exit strategies

- Valuation and liquidity

- Reducing dependency on active income

Your business can be your greatest retirement asset—or your biggest risk—depending on preparation.

Tax Efficiency in Retirement Planning

Taxes do not disappear in retirement. In some cases, they become more complex.

Smart planning focuses on:

- Tax-diversified income sources

- Strategic withdrawals

- Minimizing unnecessary tax exposure

Every dollar saved in taxes is a dollar that extends your retirement freedom.

Common Retirement Planning Mistakes to Avoid

- Starting too late

- Underestimating longevity

- Ignoring inflation

- Overconfidence in pensions or business income

- Failing to update plans as life changes

Retirement planning is not a one-time task. It is an ongoing process.

The CEO Mindset: Treat Retirement Like a Long-Term Project

Successful leaders plan long-term. Retirement deserves the same mindset.

Approach it like a business strategy:

- Set clear goals

- Measure progress

- Adjust when conditions change

- Stay disciplined

Financial independence is built through intention, not luck.

Final Thoughts: Retirement Is About Choice

Retirement planning is not about fear. It is about freedom.

When done well, it gives you:

- Control over your time

- Confidence in your finances

- Peace of mind for you and your family

The best time to plan for retirement was yesterday. The second-best time is today.

Your future self will thank you.

End of article.

Summary:

In life, nothing is permanent in this world. Everything that comes will definitely go. That is why it is best to put our best foot forward and save more for the future. The best thing that you have to start with is to have a retirement plan.

Some wait to long before they decide to plan for their future. This is not a good idea because we can never tell what lies ahead. So, here’s how and when to start retirement planning:

- The retirement year.

First, decide on what…

Keywords:

retirement planning,retirement

Article Body:

In life, nothing is permanent in this world. Everything that comes will definitely go. That is why it is best to put our best foot forward and save more for the future. The best thing that you have to start with is to have a retirement plan.

Some wait to long before they decide to plan for their future. This is not a good idea because we can never tell what lies ahead. So, here’s how and when to start retirement planning:

- The retirement year.

First, decide on what year you would like to retire. It is always best to start something with a goal in hand. This will keep you focused and determined to push it through.

- Do your homework.

The best way to help you start making your retirement planning is to consult your �employer-sponsored 401(k) or IRA,� or to any of your retirement schemes and investigate on the objective date of your mutual funds and see if it matches your target date of retirement. If it does, then start funding your nest egg immediately.

- Backups.

There are many instances where your plan can backfire. So, it is best to have backups.

So, when making a retirement plan, better include a backup that will serve as a fallback in case your nest eggs fails or if something else goes wrong. It is best that you do not depend entirely on your funds because sometimes there are circumstances that are beyond our control.

- Opt for annuities.

When doing a retirement planning, you should take note also of the different retirement planning strategies that will surely make your plan work. One good example of a retirement planning strategy is the annuities.

Basically, annuities are adaptable indemnity bonds that are exclusively patterned to bestow additional wages at the same time assist you accomplish �long-term� saving goals.

These annuities are the �long-term� items recommended by most insurance companies, though, there are brokers and other financial establishments that provide this kind of service. They will help you set-up a specific goal and aim for it.

There are two types of annuity: the immediate and the tax-deferred annuity.

In the immediate annuity, you start your retirement planning by giving a hefty amount of money to the insurance company or any financial institution for that matter. After which, your payment scheme will start at once. This type of annuity is usually applicable to those who are already 60 years old and above.

On the other hand, the tax-deferred annuities you may choose whether you will pay the retirement amount instantly or make a monthly disbursement until the time you reach your target date.

This is usually appropriate to those who start their retirement planning early, generally those who are 20 years old at the least.

- Consider the Modified Endowment Contracts.

Annuities had been heading the limelight for so many years now. Most people would go for annuities, as this is the most popular retirement planning strategy. However, like most plans, it is still vulnerable to problems and crisis. That is why, it is best to make an alternative option when making a retirement planning.

The next best retirement planning strategy is the Modified Endowment Contract or the MEC. This is, basically, one kind of �insurance policy.�

In reality, MEC is similar to annuity, especially the tax-deferred annuity, in terms of the preliminary premium rates. Though, they differ in terms of tax codes.

In annuity, the tax code appears to be very unfavourable especially when the benefactor dies while the �annuity accumulation� stage is in full force. This, in turn, makes the deferred wage taxes on development suddenly becomes payable.

In contrast, the MEC resolves this problem by providing the benefactor or the beneficiaries with an �insurance rider� included in the agreement. The �insurance rider� is made to hand over the full amount to your recipients absolutely free from any taxes.

Moreover, MECs can give you the suppleness of choosing between the variable and fixed account preferences. This, in turn, will make your retirement planning relatively easier.

Nevertheless, whatever retirement planning strategy you choose, the bottom line is that it is really important to save for your retirement as soon as possible.

Most often than not, people linger on a little longer before they start making their retirement planning. This should not be the case because you can never tell what will happen next.

As they say, life is suspense; you will never know what it can offer you until the end. So, the best time to do retirement planning is now.

Tinggalkan Balasan